First Quarter, 2026

Click here for a printable version of the Investment Update.

Listen to our latest Investment Update on Apple Podcasts, Pandora or Spotify.

Even before the jolt of the Iran conflict, investors were beginning to grapple with several new market realities: higher structural inflation, persistently higher long-term interest rates, growing skepticism about artificial intelligence (AI) and stress in private credit. At Chevy Chase Trust, we have been focused on these dynamics for some time, working diligently to position clients well amid a sea change in the economy and markets.

NAVIGATING A SEA CHANGE

The first quarter reminded investors that markets can appear calm—until they are not. The widening Middle East conflict and associated disruption to energy supplies pushed oil prices higher late in the quarter, contributing to a pullback in equities. Year to date, the S&P 500 generated a total return of -4.3%. Most equity markets outside the U.S. also retreated.

Unlike many investors, we do not view this pullback as “just another temporary shock” that inevitably sets up the next leg of the long bull market. In our view, the U.S. economy is operating under a new set of constraints. Recent events in the Middle East have brought these into stark relief. After two decades of generally disinflationary tailwinds, policymakers have less room to cut rates or add fiscal stimulus without risking inflation. That changes how markets behave—and how we manage risk.

We expect a relief rally if tensions in the Middle East ease. However, we believe the rebound may be smaller and shorter than many investors anticipate. Several economically sensitive areas of the market were already weakening, and inflation and bond yields were relatively elevated even before the Iran conflict began.

The risks are substantial. It has been a long time since inflation was a persistent problem in the U.S. Many asset managers have never invested during an inflationary environment. This quarter’s volatility reinforced why diversification, valuation discipline and a focus on durable long-term investment themes matter.

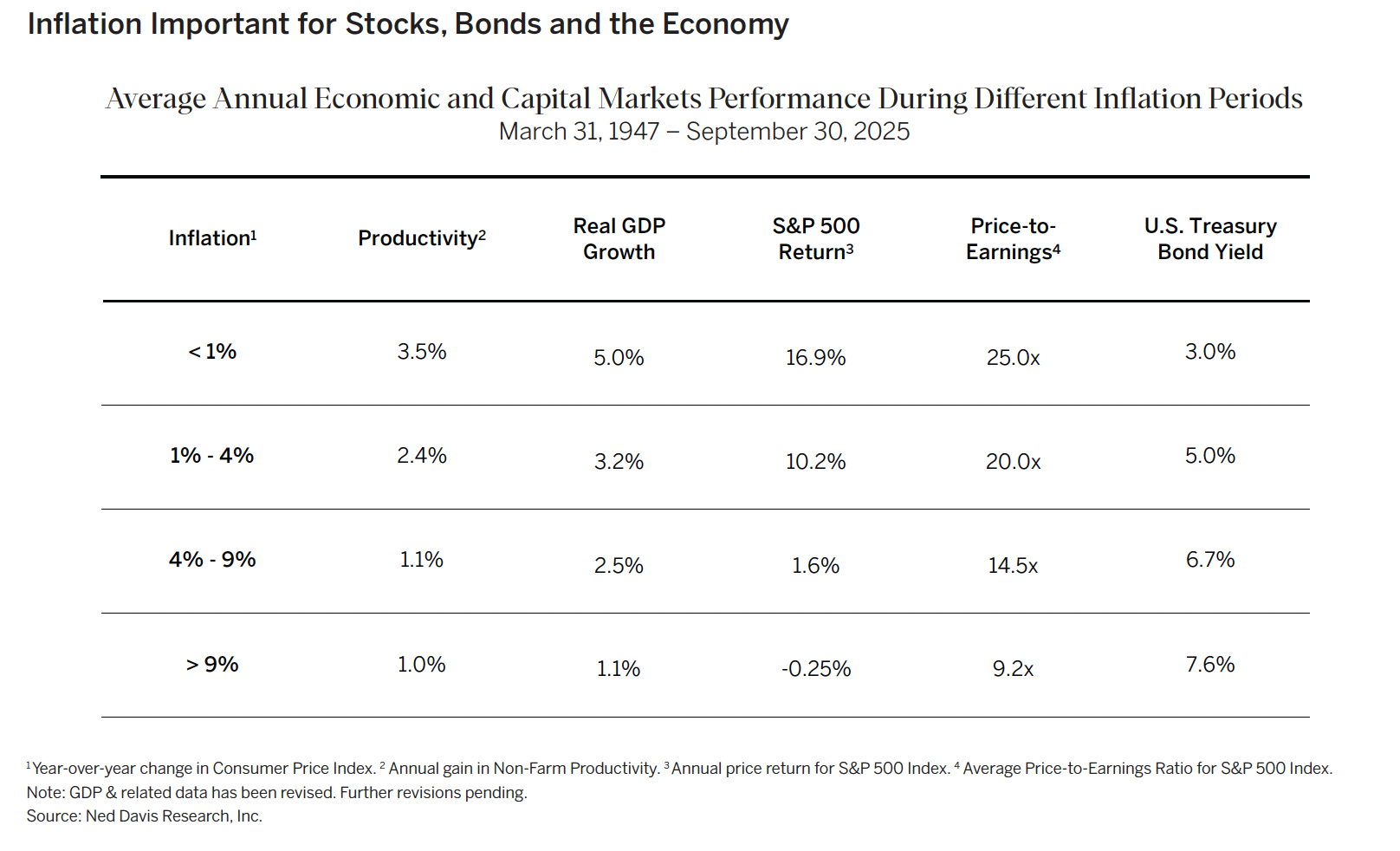

INFLATION MATTERS MORE THAN MANY INVESTORS APPRECIATE

Inflation is arguably the most important macroeconomic factor influencing the direction of financial markets— and the economy itself. When inflation is very low, real economic growth is typically stronger and corporate valuations tend to be higher. Conversely, when inflation is high, real growth typically slows, lenders demand higher interest rates and stock valuations usually compress.

The display below shows that periods of higher inflation have tended to coincide with weaker productivity and slower real economic growth. In all but the most extreme cases, stocks still delivered positive returns over time. However, the price investors are willing to pay for earnings (expressed by the P/E ratio) has usually been lower, and bond yields have generally been higher. In other words, higher inflation often means a tougher environment for both stocks and bonds.

POLICY MAKERS HAVE LESS ROOM FOR RESCUE

For most of the last 20 years, a set of broad global forces – China’s entry into the World Trade Organization (WTO), the globalization of supply chains, a surge of cheap energy from U.S. shale production and rapid adoption of new technologies with quickly falling prices – kept inflation low. This was particularly true in the United States, where companies more aggressively capitalized on these trends. Persistent low inflation enabled the Federal Reserve and U.S. government to respond quickly and powerfully to the Global Financial Crisis and COVID shutdown.

But these disinflationary forces stalled well before the Iran war-induced energy shock began. In January, the Fed’s preferred measure of inflation(1) rose to 3.1%. It has been above the Fed’s stated 2% target for five years. As a result, policymakers are now more constrained. Easing policy via lowering interest rates or providing stimulus may increase inflation, and that limits how quickly markets can count on a rescue should one be needed.

HIGHER INFLATION AND DEBT COULD KEEP INTEREST RATES ELEVATED

Despite an epic capital markets boom and solid economic growth, U.S. federal government debt grew from $10.7 trillion at the end of 2008 to $38.5 trillion by the end of 2025. It’s now a staggering 122% of GDP.

For much of this period, interest rates were extremely low, which helped keep government debt-servicing costs manageable. Today, long-term Treasury yields are nearly double their average from 2008 through 2020, and they may rise further. The interest expense on U.S. debt now exceeds defense spending. Given the current annual deficit spending of about 6% of GDP, the situation will likely get worse.

After decades of handwringing by commentators about rising levels of U.S. government debt, markets are finally showing increased concern. Recent auctions of Treasury bonds have gone less smoothly than usual, and long-term bond yields have not fallen after Fed rate cuts.

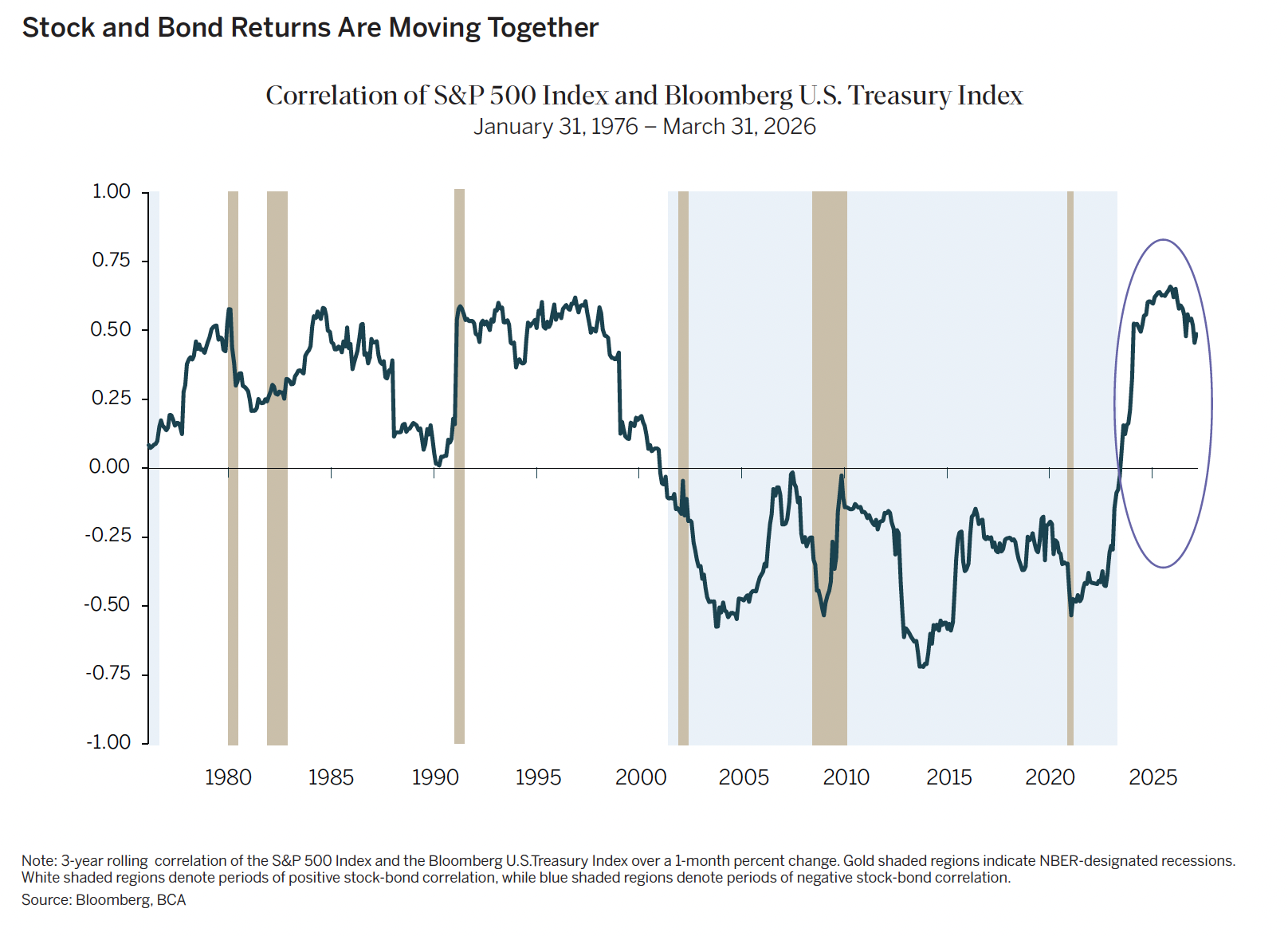

The correlation between stocks and bonds has also flipped from an inverse relationship to a positive relationship. In the last few years, when bond prices have fallen, stocks have also declined. This is a signal that the economic backdrop is different than it was for most of this century.

AI OPTIMISM IS BEING TESTED

Over the past three years, a small group of large technology companies—often called the Mag 7 (2)—has driven almost half of S&P 500 returns. In the first quarter of 2026, that group was down on average nearly 12%. The reversal of these market leaders accounted for nearly 90% of the Index’s decline in the quarter.

Since 2023, investor interest in the Mag 7 was driven largely by seemingly boundless enthusiasm for AI. Now, many are beginning to question the scale and pace of spending required to build AI infrastructure. Just four companies(3) are expected to spend more than $650 billion in 2026, on top of the $420 billion they spent in 2025. Continuing this AI infrastructure buildout will require substantial additional capital, including an increased reliance on debt financing. Higher bond yields, as described above, raise the hurdle rate for these projects and pressure valuations across the board, particularly for growth companies.

Transformative technologies can create enormous value, but the investment cycle can overshoot, especially when capital is abundant.

History offers a useful analogy. The rapid growth of Internet traffic (just under 500,000% over the last 25 years) ultimately reshaped the economy, but many early investors still reaped disappointing returns. Too much capital chased the opportunity before sustainable business models emerged. The same risk exists in parts of today’s AI buildout.

Like AI, the Internet buildout required massive capital spending, but even at the height of the dot-com boom the ratio of capital spending to revenue was far more rational than is the case today for AI. U.S. telecom companies eventually managed to squeeze profits from their Internet-related businesses, but only because equipment prices plunged. So far, AI hardware and data-center infrastructure costs have not fallen fast enough to allow the creators of large-language models and the data centers that support AI traffic to generate attractive returns on investment.

If financing costs rise at the same time that competition intensifies, today’s optimistic assumptions about AI profitability could be challenged, and major projects may be scrapped. This is one reason why we have been cautious about investing in the more crowded parts of the AI trade.

As one commentator put it, we are not only running an experiment about a powerful technology. We are also running an experiment about how much capital markets are willing to fund before returns become clear.

Recent events in the private credit market suggest that we may be testing the limits of this experiment. For much of the past decade, private credit was sold to both institutional and retail investors as a virtually “risk-free” way to earn extra yield. We frequently cautioned clients that this sales pitch was too good to be true, but many yield-seeking investors bought it. The assets of private debt managers have increased by $1 trillion over the last ten years, while traditional commercial and industrial loans in the banking system have barely grown. Much of that lending went to the Technology sector, and write-downs are building. This has prompted many investors to try to liquidate their holdings, but increasingly, managers are limiting withdrawals.

Many investors see the various market-moving issues we’ve described—the war-driven energy price shock, higher inflation and interest rates, soaring AI investment and private credit market wobbles—as distinct issues. We view them as interrelated. We are no longer investing in a world where capital is very inexpensive and where broadly disinflationary forces allow aggressive government intervention at the first sign of trouble. This changes the risk/reward calculation.

PORTFOLIO POSITIONING AND THEMATIC UPDATE

With markets beginning to reflect inflation concerns and more scrutiny of AI-related spending, several of our themes held up relatively well during the quarter. Our End of Disinflationary Tailwinds theme benefited from strength in the Energy sector and other areas that tend to perform well as inflation rises. The Energy sector outperformed the broader S&P 500 by over 40% this quarter. While we continue to see long-term opportunities in this theme, we may begin to take some profits in names that have soared, at least in part, due to the war in Iran.

We also continue to see great promise in our Opportunities Abound Abroad theme, even as the war in the Middle East created short-term headwinds for some international markets. While we are not there just yet, we think a further deterioration in relative performance may present a chance to increase positions.

Some holdings of our Next-Generation Automation and Advent of Molecular Medicine themes performed well as growth investors broadened their holdings beyond the most crowded Mag 7 and AI-related names. We think widespread adoption of AI may help both these themes over the mid- to longer-term. Many of the holdings in our Advent of Molecular Medicine theme are critical to generating the genetic data that will likely power AI’s use in the healthcare industry. Similarly, automation technologies should proliferate as AI tools are eventually applied in the physical world.

CONCLUSION: DISCIPLINED INVESTING IN A HIGHER VOLATILITY ERA

At the start of 2026, investor sentiment was broadly optimistic. This quarter’s pullback has reduced some of that optimism, but it has not changed the underlying reality. We are in a transition period shaped by geopolitics; higher structural inflation and a new relationship between stocks, bonds and policy. And all of this at a time when starting valuations and investor allocations to equities are near record highs.

In such an environment, it is especially important to avoid overconfidence and to stay focused on fundamentals. Our philosophy is straightforward: we do not make heroic, headline-driven bets in areas where we believe our thematic research doesn’t give us an edge. We cannot know the timing of diplomatic breakthroughs or the next turn in a conflict or when the market’s embrace of AI and private credit will loosen.

Instead, we focus on managing risk deliberately, diversifying exposures and investing in well-researched themes that we believe offer long-term return potential that is underappreciated by the market. We are grateful for the trust you place in us as we do this.

(1) Core personal consumption expenditure (“Core PCE Index”)

(2) The Mag 7 are Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla.

(3) The four hyperscalers are Microsoft, Amazon, Google and Meta. Other firms, such as Oracle and Open AI, are spending heavily but are not included in the totals above.

Important Disclosures This commentary is for informational purposes only. The information set forth herein is of a general nature and does not address the circumstances of any particular individual or entity. You should not construe any information herein as legal, tax, investment, financial or other advice. Nothing contained herein constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments. This commentary includes forward-looking statements, and actual results could differ materially from the views expressed. Materials referenced that were published by outside sources are included for informational purposes only. These sources contain facts and statistics quoted that appear to be reliable, but they may be incomplete or condensed and we do not guarantee their accuracy. Fact and circumstances may be materially different between the time of publication and the present time. Clients with different investment objectives, allocation targets, tax considerations, brokers, account sizes, historical basis in the applicable securities or other considerations will typically be subject to differing investment allocation decisions, including the timing of purchases and sales of specific securities, all of which cause clients to achieve different investment returns. Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment or investment strategy will be profitable, equal any historical performance level(s), be suitable for the portfolio or individual situation of any particular client, or otherwise prove successful. Investing involves risks, including the risk of loss of principal. The level of risk in a client’s portfolio will correspond to the risks of the underlying securities or other assets, which may decrease, sometimes rapidly or unpredictably, due to real or perceived adverse economic, political, or regulatory conditions, recessions, inflation, changes in interest or currency rates, lack of liquidity in the bond markets, the spread of infectious illness or other public health issues, armed conflict, trade disputes, sanctions or other government actions, or other general market conditions or factors. Actively managed portfolios are subject to management risk, which involves the chance that security selection or focus on securities in a particular style, market sector or group of companies will cause a portfolio to incur losses or underperform relative to benchmarks or other portfolios with similar investment objectives. Foreign investing involves special risks, including the potential for greater volatility and political, economic and currency risks. Please refer to Chevy Chase Trust’s Form ADV Part 2 Brochure, a copy of which is available upon request, for a more detailed description of the risks associated with Chevy Chase Trust’s investment strategy. The recipient assumes sole responsibility of evaluating the merits and risks associated with the use of any information herein before making any decisions based on such information.