We are proud to announce that Chevy Chase Trust has been ranked on the Forbes 2025 list of America’s Top RIA Firms.

This recognition reflects our continued commitment to putting clients and their success first.

The Forbes ranking, developed by SHOOK Research, considers both qualitative and quantitative factors, including due diligence interviews, assets under management, compliance records, and best practices.

We are grateful to our clients for their continued trust and to our team for their dedication.

Congratulations to Deb Gandy, Senior Managing Director at Chevy Chase Trust, on being recognized with the Virginia Women in Leadership Award by Virginia Business magazine!

This prestigious award celebrates 45 outstanding women executives for their overall professional accomplishments, civic engagement, mentorship and breaking glass ceilings.

The event was held at the historic Jefferson Hotel in downtown Richmond, VA. In attendance to celebrate Deb were colleagues Jeff Whitaker, CEO and President, Stacy Murchison, Chief Marketing Officer, Laly Kassa, Co-Head of Planning Group, Marc Wishkoff, Head of Business Development and Ramona Mochovia, Senior Managing Director.

The award was announced in July 2025 based on lifetime achievement and was presented on October 6, 2025. Chevy Chase Trust paid no application fee to participate.

We’re proud to share that Chevy Chase Trust has been named to CNBC’s 2025 Financial Advisor 100 list.

CNBC’s Financial Advisor 100 list recognizes the best financial advisors and firms that help clients successfully navigate their financial lives. It is based on data analysis and editorial review, evaluating factors such as assets under management, firm size and longevity, number of certified financial planners and regulatory records.

This recognition reflects our continued commitment to delivering thoughtful and client-centered service. We are grateful to our clients for their trust and partnership.

As capital markets extend a remarkable but volatile streak of strong performance, we explore the headwinds and tailwinds being navigated by U.S. companies and explain how we are adjusting portfolios to find opportunity amid rapid change. We also share our perspective on recent developments in private equity.

A QUARTER OF STRONG RETURNS BUT GROWING UNCERTAINTY

The U.S. equity markets continued to defy gravity in the third quarter of 2025. The S&P 500 delivered a total return of 8.1% in the quarter, bringing its year-to-date return to 14.8%. Non-U.S. equity markets were also strong, with the MSCI EAFE Index1 generating a total return of 4.9% in the third quarter and an impressive 25.8% year to date. During the third quarter, U.S. equities were buoyed by:

Solid second-quarter earnings results, which exceeded lowered expectations

The prospect of interest rate cuts, the first of which took place in September

Easier financial conditions, due to higher stock prices and a continued slide in the U.S. dollar, which contributed to the earnings growth noted above

Optimism about tax cuts and fiscal stimulus resulting from the One Big Beautiful Bill Act (“OBBBA”)

Continued torrential corporate spending on Artificial Intelligence (“AI”) infrastructure around the country

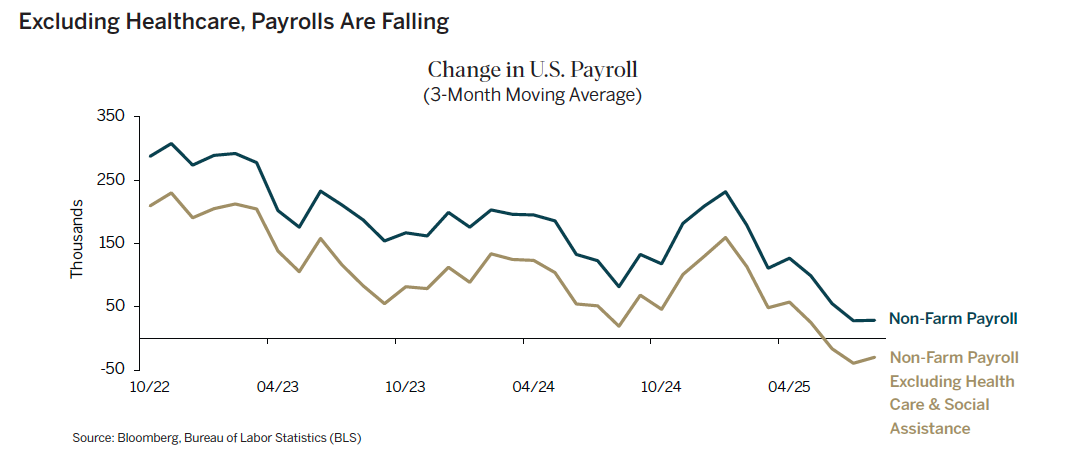

The Atlanta Fed’s GDPNow model projects U.S. Gross Domestic Product (“GDP”) growth was a strong 3.8% in the third quarter. Nonetheless, employment growth has decelerated sharply. Excluding the less economically sensitive health care sector, the three-month moving average in private payrolls fell by 30,000 in August.

How can we reconcile this unusual discrepancy between solid U.S. GDP growth and weak employment? By definition, GDP growth equals employment growth times productivity growth. Therefore one of three scenarios must unfold:

A long-awaited productivity boom could develop. AI or increased digital investment made during the pandemic could be contributing to economic growth without employment growth. This would be the best outcome for U.S. equities, because if continued, it could usher in a sustained disinflationary boom. However, surveys of companies using AI do not show this to be the case yet. A recent McKinsey poll found that, while almost 80% of companies are now using generative AI, the vast majority have not seen a bottom line benefit from it. Another study by researchers at MIT found that 95% of companies have seen no gains from their AI investments.

Employment growth could catch up to GDP growth. This scenario would have mixed implications for stocks. On the one hand, concerns about rising unemployment would fade. On the other hand, stronger demand for labor could push up wages, fueling inflation, which has remained stubbornly above the Fed’s 2% target. Higher inflation could, in turn, keep the Fed from cutting rates as much as the market currently expects, disappointing investors.

Employment growth could remain low and economic growth could slow. Falling or flat demand for labor, coupled with nearly 3% inflation, would cause real income growth to be weak. With pandemic savings largely depleted, consumer loan delinquency rates up and home prices no longer rising, slow income growth could cause consumer spending to stumble, tipping the economy into recession. This would be the worst-case scenario for stocks. Given the widespread ownership of equities in the U.S., even a relatively small decline in equity prices could lead to a meaningful pullback in spending, thereby creating a negative feedback loop, in which lower equity prices lead to lower consumption, which then causes equity prices to fall further.

High valuations and widespread investor optimism lead us to believe that most people are betting on Scenario 1. We think the odds are greater that either Scenario 2 or 3 unfolds.

CAN U.S. CORPORATE EXCEPTIONALISM CONTINUE?

While the U.S. economy has grown faster than other high-income economies in recent decades, U.S. companies have increased their profitability even faster than economic growth alone would suggest. The magnitude of U.S. earnings growth has been integral to the record 25 years of U.S. equity market outperformance.

For global investors, determining whether U.S. outperformance can continue is of paramount importance, especially now, when U.S. policy changes may reduce some tailwinds that helped U.S. companies achieve these spectacular results.

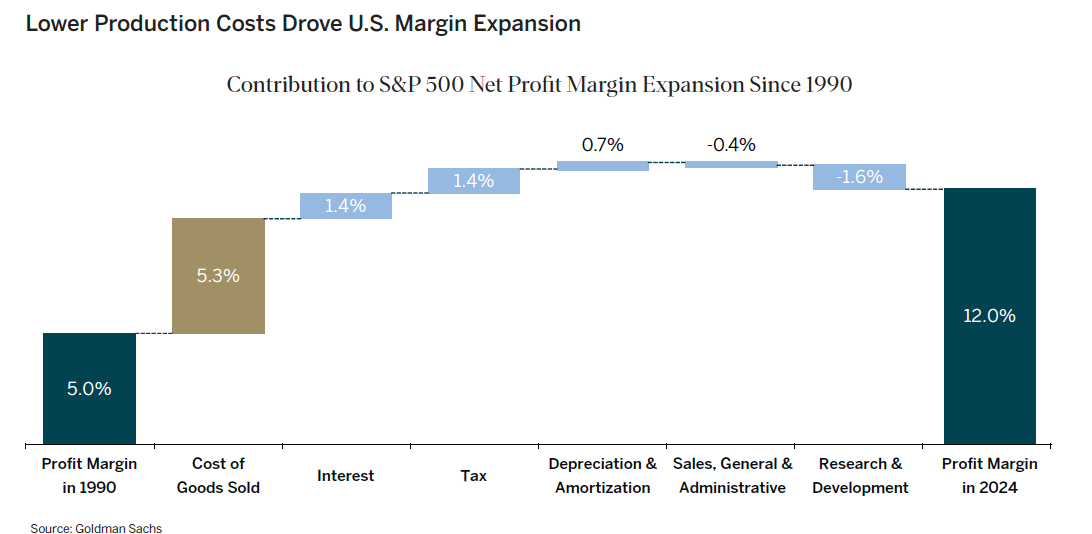

Since 1990, several factors drove the exceptional margin expansion of U.S. companies.

While lower interest costs and taxes helped, the biggest contributor to margin expansion was the reduction in the cost of goods sold (“COGS”), an accounting term for the cost of production. A good deal of this cost reduction came from outsourcing labor- and resource-intensive operations to regions with lower costs of labor, energy and land. Access to a low-cost, global work force led to lower U.S. wage growth and allowed companies to produce and sell goods at lower prices. This contributed to significantly lower levels of inflation, which reduced interest rates and supported the lower levels of interest expense shown above.

Stricter labor laws, regulations and other policies in Europe and Japan prevented corporations based in those areas from globalizing operations to the same extent and kept domestic input and labor costs relatively high.

Can U.S companies continue to grow margins at a faster rate than other developed markets? We see several tailwinds that may support continued margin improvement, but a larger set of headwinds that will make it hard for U.S. companies to repeat the profit improvements of the past.

Two tailwinds stand out. First, U.S. taxes will almost certainly come down. The average effective U.S. corporate tax rate is projected to fall to around 10% next year due to OBBBA provisions. Second, the Administration’s efforts to encourage capital spending, through accelerated depreciation, reduced environmental regulation and bank regulatory reform, could help companies boost profits.

However, it is unclear whether these efforts will be enough to offset several meaningful headwinds. First, interest costs for corporations are likely to rise in future years as debt issued when interest rates were extremely low matures and is refinanced at higher rates.

Second, and of greater significance, the Administration’s policies that are intended to bring manufacturing back to the U.S. will make further improvements in COGS difficult. Direct tariff costs and the slowing or reversal ofoffshoring are likely to increase total production costs. Even if offshoring persists, wages are rising in China and other places where companies had moved operations, leaving fewer opportunities to cut costs by moving production abroad.

While the national security and supply chain resiliency benefits of domestic production are important, it is worth noting that in recent decades, Japan and Germany have not derived stronger economic growth or superior corporate profitability from policies supporting a large domestic manufacturing base.

It is possible that AI may begin to improve productivity and efficiency, boosting profitability, but we believe this is further in the future than many think. Our best guess is that management teams may be able to sustain current high margins but will have trouble expanding margins materially from this peak. If this is the case, investors are likely to be disappointed as sales growth alone is unlikely to meet the lofty earnings expectations embedded in current stock prices.

OUR INVESTMENT THEMES

Ironically, just when the U.S. appears to be taking a less laissez-faire approach to industrial policy, many other countries are moving in the opposite direction. Many of the policies outlined in Mario Draghi’s recent report on European Union competitiveness are explicitly designed to improve European profit margins by reducing barriers to intra-European trade and by lowering input and borrowing costs.

We’ve discussed our Opportunities Abound Abroad theme in many of our recent Investment Updates. Non-U.S. equity markets have performed quite well this year, and valuations in many non-U.S. geographies still look very attractive at a time when U.S. equities are arguably priced for perfection. We continue to lean into this theme.

We have recently been adding to our End of Disinflationary Tailwinds theme. Fiscal and monetary policies in almost all major economies are loose, which should support consumption globally. And if we do get a productivity boost from AI or elsewhere, wealth will increase, and consumers will consume even more than they do today.

Relatively low oil prices have led to a significant reduction in capital investment by energy companies. After OPEC brings its current spare capacity online, most likely over the next 12-18 months, easily accessible energy reserves will decline dramatically. Investors are clearly not focused on this eventuality now, but we believe the lack of investment today will lead to meaningfully higher prices in the future. We’re slowly beginning to position for this eventuality by increasing our energy sector holdings at a time when we believe these stocks are relatively cheap and unloved.

IN CONCLUSION

We find ourselves at a moment of unprecedented change and uncertainty, where there are a broad range of possible economic and market outcomes. The industrial policies of the U.S. and many other economies are becoming more mercantilist. Corporate investment in AI remains unabated despite limited commercial benefits thus far. We are navigating this moment with discipline, adjusting portfolios as opportunities emerge. We are also making sure to adhere to and continuously refine our time-tested approach to Thematic research and investing, which we believe will continue to serve clients well.

(1) The MSCI EAFE Index is an equity index that captures large and mid-cap representation across 21 developed markets countries (Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the UK). The Index excludes the US and Canada.

BEWARE GREEKS BEARING GIFTS: THE “DEMOCRATIZATION” OF PRIVATE EQUITY

Private Equity (“PE”) funds have long been portrayed as the Rolls Royces of the investment world. With typical minimum investments of $5 million or more, PE has been the exclusive preserve of ultra-wealthy families and the largest institutions. And rightly so. Few investors have the financial wherewithal and long investment horizon needed to accept the lack of liquidity, transparency and decision rights in this asset class.

But now, some of the biggest names in PE are throwing open their doors to anyone who can make a minimum investment of $25,000 in a new class of retail-oriented funds, an effort trumpeted as “democratizing” PE.

One can’t help thinking of the Greek army’s gift of a large wooden horse to the city of Troy in The Aeneid. PE managers aren’t welcoming the public into this asset class to be kind. They created these new retail funds in response to poor recent investment performance, lengthening periods of illiquidity and challenging fund manager economics.

DISAPPOINTING PERFORMANCE

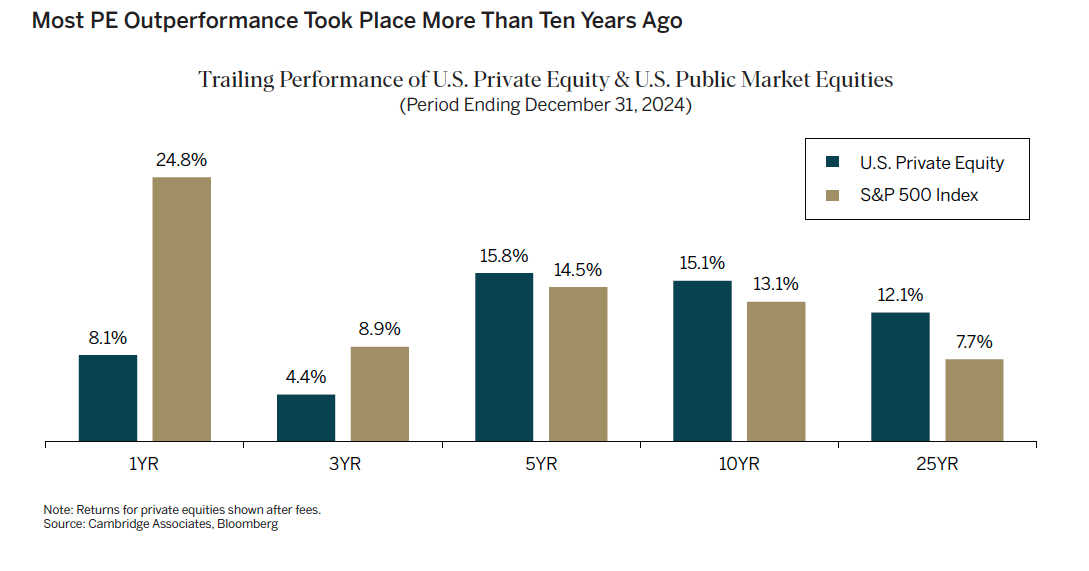

Long-time investors are dissatisfied with recent PE returns and increasingly concerned that future returns may be no better. As of the end of 2024, PE as a category had underperformed the S&P 500 after fees over the one- and three-year periods and delivered returns close to public equity indices over the five- and ten-year periods. While PE did materially beat the S&P 500 over a 25-year period, most of that outperformance occurred in the early part of that long time span.

What went wrong? As is often the case on Wall Street, early success led to too much money chasing too few opportunities. PE emerged as a small but prominent asset class in the 1980s. Functioning basically as leveraged value investors, PE funds used debt to buy controlling interests in companies at low prices, with the goal of selling them at much higher prices after improving operations or breaking them up to capture the value of their parts.

Despite some spectacular failures – most notably KKR’s $25 billion buyout of RJR Nabisco in 1989, which lost roughly $730 million over 15 years – many early PE investments generated hefty returns. The success of early adopters, such as the Yale University endowment, attracted other institutional investors, leading to an explosion in PE assets under management. PE grew from roughly $600 billion in 2000 to almost $10 trillion in 2024, with another $2 trillion in contractually committed capital.

PE is no longer a niche, nimble asset class, and it becomes much harder to earn a high return on investment after the amount of capital to invest increases more than 15-fold.

To deploy ever greater pools of capital, PE firms have been forced to do bigger deals. In 2009, only 4% of PE deals in North America were valued at greater than $1 billion. In 2024, $1 billion-plus deals accounted for 22% of transactions.

The pressure to invest has also driven up valuations at purchase. In 2009, PE firms were buying companies at average multiples that were 40% below multiples for comparable public equities. That discount has narrowed over the past three years to less than 5%.

In late September, a consortium led by Silver Lake and Saudi Arabia’s Public Investment Fund announced the $55 billion purchase of Electronic Arts (“EA”), a video game maker, setting a record for the largest PE transaction ever. The purchase price represents a 25% premium to EA’s closing share price on NASDAQ the day before deal talks were reported by The Wall Street Journal.

Complicating matters further, the increased cost of debt to fund purchases is not just an additional drag on investment returns. Higher debt levels increase the risk of portfolio company bankruptcy at times of economic stress.

LIQUIDITY PRESSURES

Institutional investors in PE are facing a liquidity crunch due to a three-year-long drought in distributions. With the decline in M&A activity and initial public offerings in recent years, PE funds have struggled to exit investments. On average, they are holding investments longer. These longer holding periods both lower annualized returns and delay distributions to investors.

For endowments, the liquidity strain is particularly difficult to tolerate. Many universities and other entities now face uncertain government funding, increased tax exposure and challenging enrollment and tuition trends. As a result, many are now selling some of their private equity stakes at a discount in the secondary market to gain liquidity. Secondary market activity has nearly tripled in value over the past four years.

MANAGERS NEED ASSET GROWTH

Traditional PE fundraising has declined in each of the past three years, limiting the growth in assets under management. Without ample new capital, PE funds may not have the revenue growth needed to support current investments and attract, retain and compensate the investment professionals and operating partners they need to identify new investment targets and create value in portfolio companies.

NOW ENTER “DEMOCRATIZATION”

That’s where “democratization” and the new retail funds come in. Wall Street is looking for a new revenue stream, using the elite reputations of PE managers to sell PE retail funds to the masses. PE managers, in turn, are seeking to grow assets under management, revenues and profits. And legacy PE investors are hoping to gain the liquidity they need by selling old investments to these new retail funds.

While we believe that many PE investors stand to make money in the coming decades, outsized returns are likely to be far harder to come by than in the early days of the asset class. Only those clients that can handle prolonged periods of illiquidity and tolerate the category’s opacity and lack of control should delve into PE investing. And perhaps more than ever, careful manager and vehicle selection will be key to avoiding the modern financial equivalent of a Trojan Horse.

Important Disclosures This commentary is for informational purposes only. The information set forth herein is of a general nature and does not address the circumstances of any particular individual or entity. You should not construe any information herein as legal, tax, investment, financial or other advice. Nothing contained herein constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments. This commentary includes forward-looking statements, and actual results could differ materially from the views expressed. Materials referenced that were published by outside sources are included for informational purposes only. These sources contain facts and statistics quoted that appear to be reliable, but they may be incomplete or condensed and we do not guarantee their accuracy. Fact and circumstances may be materially different between the time of publication and the present time. Clients with different investment objectives, allocation targets, tax considerations, brokers, account sizes, historical basis in the applicable securities or other considerations will typically be subject to differing investment allocation decisions, including the timing of purchases and sales of specific securities, all of which cause clients to achieve different investment returns. Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment or investment strategy will be profitable, equal any historical performance level(s), be suitable for the portfolio or individual situation of any particular client, or otherwise prove successful. Investing involves risks, including the risk of loss of principal. The level of risk in a client’s portfolio will correspond to the risks of the underlying securities or other assets, which may decrease, sometimes rapidly or unpredictably, due to real or perceived adverse economic, political, or regulatory conditions, recessions, inflation, changes in interest or currency rates, lack of liquidity in the bond markets, the spread of infectious illness or other public health issues, armed conflict, trade disputes, sanctions or other government actions, or other general market conditions or factors. Actively managed portfolios are subject to management risk, which involves the chance that security selection or focus on securities in a particular style, market sector or group of companies will cause a portfolio to incur losses or underperform relative to benchmarks or other portfolios with similar investment objectives. Foreign investing involves special risks, including the potential for greater volatility and political, economic and currency risks. Please refer to Chevy Chase Trust’s Form ADV Part 2 Brochure, a copy of which is available upon request, for a more detailed description of the risks associated with Chevy Chase Trust’s investment strategy. The recipient assumes sole responsibility of evaluating the merits and risks associated with the use of any information herein before making any decisions based on such information.

Investing Beyond Borders: The Case for Developed Markets Abroad

Thematic Research Analyst Zachary Navarroexplains how the theme demonstrates Chevy Chase Trust’s ability to uncover overlooked investment opportunities.

Could you provide an overview of the ‘Opportunities Abound Abroad’ theme?

This theme reflects our conviction that developed markets outside the United States — particularly in Europe and Japan — are likely to exceed expectations. While U.S. markets have led global returns for more than a decade, changing geopolitics as well as structural reforms in fiscal, energy and industrial policies are taking hold in Europe and Japan. These changes, combined with more attractive valuations, could drive stronger equity performance abroad and present compelling opportunities for long-term investors.

Can you provide more details on the developments driving these changes?

In Japan, the Tokyo Stock Exchange (TSE) has introduced regulatory changes that encourage mergers and acquisitions, as well as greater returns to shareholders, through dividends and buybacks. Further, inflation has picked up modestly, allowing the Bank of Japan to implement positive interest rates for the first time in nearly a decade. In Europe, post-Sovereign Debt Crisis reforms have made banking systems more resilient, while strengthened cooperation amongst EU Member States is breaking down internal barriers. Furthermore, significant shifts in fiscal policy are allowing for more debt to support higher levels of spending on infrastructure, research and development and defense. These structural changes improve the investability of those markets.

What prompted Chevy Chase Trust to research this area?

The genesis of this theme was a valuation discrepancy that we began tracking some time ago. U.S. stocks were trading at historically high multiples — far above their 10-year averages — while non-U.S. developed market multiples were in line with or even below their historical valuations. We began to question whether the valuation discrepancies were warranted going forward, given the structural changes we were beginning to see in Japan and Europe. The disconnect between market perception and economic reality — paired with the U.S. vs. non-U.S. valuation gap — became too compelling to ignore.

Can you walk us through the process of creating a new theme, using Opportunities Abound Abroad as an example?

This theme began with our macroeconomic research process. Each week, we review extensive data and analysis — everything from economic indicators to geopolitical developments. When we see a shift happening, we dig deeper to assess whether it’s investable. In this case, we started with an observation — that U.S. valuations were high compared to other developed markets — and sought to understand why this was and what might change. During our work, we identified desirable structural changes underway in certain developed markets outside the U.S. that convinced us that the past valuation differences between the U.S. and non-U.S. markets weren’t likely to persist longer term. From there, we identified specific companies that stood to benefit from those changes. Once we determined the opportunity was large enough to represent a meaningful portion of the portfolio, it became a formal theme — one that we announced in the second quarter of 2023.

How does this theme reflect Chevy Chase Trust’s Global Thematic Investing approach?

This is a textbook example of our process. We start with technological, scientific, demographic or macroeconomic shifts — in this case, the changing dynamics in Japan and Europe — and work through the implications for companies and industries. We don’t just respond to headlines. We conduct extensive, proprietary, in-depth research, assessing long-term viability and asking whether there’s enough breadth and depth to build a diversified theme consisting of investment opportunities across different sectors and regions. If there is, and the valuation case is strong, we’re ready to invest.

How has this theme evolved in the past two years? Where do you see it going in the future?

At first, we focused on the structural reforms happening in Europe and Japan. Over time, those reforms have accelerated — Germany has significantly shifted its stance on debt, NATO countries are boosting defense spending, and trade barriers within the EU have continued to fall. In Japan, mergers and acquisitions are at all-time highs with returns to shareholders climbing as Japanese companies change their attitude on buybacks and dividends. Meanwhile, U.S. valuations have risen even higher above historical averages. Going forward, we anticipate the valuation gap could narrow through some combination of international valuations improving and/or U.S. valuations contracting. Valuations abroad should rise as investors appreciate the changes made by the TSE to make Japanese firms more attractive, or as European economies benefit from common debt issuance, more fiscal stimulus and the reduction of internal barriers. Meanwhile, U.S. valuations may be reduced as investors consider the long-term profitability of artificial intelligence investments or the U.S. fiscal position.

How are current U.S. policies and economic uncertainty impacting this theme today?

Some of the more protectionist policies we’ve seen recently in the U.S. are adding friction to global trade — but they’re not reversing globalization. Instead, they’re forcing supply chains to adapt. Goods that once came directly from China might now be routed through Vietnam or Indonesia to lower tariff rates. This reconfiguration creates inefficiencies and raises costs.

Further, U.S. tariffs should result in lower domestic import demand and may lead to global manufacturing overcapacity. In the near term, this overcapacity should result in lower prices in non-U.S. markets. Over a longer horizon, politicians may attempt to solve manufacturing overcapacity by either producing fewer goods or encouraging higher levels of consumption. We believe the former would likely result in a global recession while the latter would result in more balanced growth with a greater share generated in non-U.S. markets.

At the same time, rising deficits and spending constraints in the U.S. may limit economic growth and hamper innovation as government funded R&D is sacrificed due to the rising cost of servicing the national debt. In contrast, many developed markets abroad are breaking down trade barriers, embracing investment and fostering economic cooperation — all of which we believe bode well for this theme.

What questions are you hearing from clients about this theme?

Lately, the biggest question we get is whether the theme is already fully valued. The short answer is no. In fact, the valuation gap between U.S. and non-U.S. developed markets has widened even further in the past quarter. We track that data closely and see room for international markets to continue their recent outperformance. Overall, we believe the structural reforms and economic shifts underway are still in the early innings. As these fundamentals continue to take hold, we expect this theme to continue to play out.

We’re pleased to announce that Chevy Chase Trust has been named to Barron’s 2025 Top 100 RIA Firms list — a prestigious recognition we’ve consistently earned since 2019. The Barron’s Advisor’s ranking considers both quantitative and qualitative measures – such as assets managed, growth, technology spending, size, shape and diversity of the team and compliance records. We know that our success is a direct result of the trust our clients place in us and the dedication of our exceptional team.

Click here to read more about this year’s rankings.

Barron’s rankings were awarded on September 15, 2025 for data as of June 30, 2025. Chevy Chase Trust paid no application fee to participate.

Chevy Chase Trust is proud to share thatDeb Gandy, Senior Managing Director, has been named one ofNorthern Virginia Magazine’s 2025 Top Financial Professionals.

This recognition highlights Deb’s expertise, dedication, and the trust she’s earned from clients and peers alike. We celebrate her leadership and commitment to delivering thoughtful, client-focused financial strategies.

Northern Virginia Magazine’s 2025 Top Financial Professionals were awarded on 5/8/2025, based on the reader survey conducted from 3/10/2025 through 3/31/2025. No fees were paid to participate.

The recently passed One Big Beautiful Bill Act (OBBBA) includes changes to the charitable contribution deduction. Beginning January 1, 2026, taxpayers will be subject to a new floor on the charitable deduction and a cap on their total itemized deductions. There is therefore a short window between now and December 31st to take another look at your charitable goals to maximize the benefits of your donations prior to the changes in the law.

Floor on Charitable Contributions

After 2025, the itemized deduction for charitable contributions will be subject to a reduction equal to 0.5% of a taxpayer’s Adjusted Gross Income (AGI). This floor is applicable to all levels of AGI, all filing statuses, all charitable contribution amounts, and is in addition to the existing caps on charitable contributions (more on the caps a bit later).

For example, in 2026, a taxpayer with AGI of $1,000,000 will have $5,000 ($1,000,000 * .005) subtracted from their charitable deduction. If the individual donates $300,000 to charity, the taxpayer’s deduction will be reduced to $295,000. Since the floor is determined by the taxpayer’s AGI and is regardless of the amount contributed, this taxpayer will have the same $5,000 reduction whether the donation is for $10,000, $300,000 or any other amount.

Cap on Total Itemized Deductions

The OBBBA also caps the tax benefit of total itemized deductions for taxpayers subject to the 37% tax bracket. This cap effectively limits the benefit of itemized deductions to a maximum 35% tax rate. After 2025, total itemized deductions for taxpayers in the 37% bracket will be reduced by 2/37 of the lesser of (a) the taxpayer’s total itemized deductions, or (b) the excess of taxable income plus total itemized deductions over the 37% bracket threshold. The 37% bracket amount for 2025 starts at taxable income of $626,351 for single and head of household filers or $751,601 for married taxpayers filing jointly. The threshold amounts are adjusted for inflation each year and are expected to increase for 2026.

For example, in 2026, assume married taxpayers have a combined AGI of $1,000,000, a charitable contribution deduction of $295,000 (for their donation of $300,000) and a $10,000 deduction for State and local taxes, for total itemized deductions of $305,000. The preliminary taxable income is $695,000 ($1,000,000 – $305,000). Using the threshold amounts for 2025, the taxpayers’ itemized deductions would be reduced by $13,427, which represents the lesser of (a) ($305,000 * 2/37) = $16,486 or (b) ($695,000 + $305,000 – $751,600) * 2/37) = $13,427. Total itemized deductions are therefore reduced from $305,000 to $291,573.

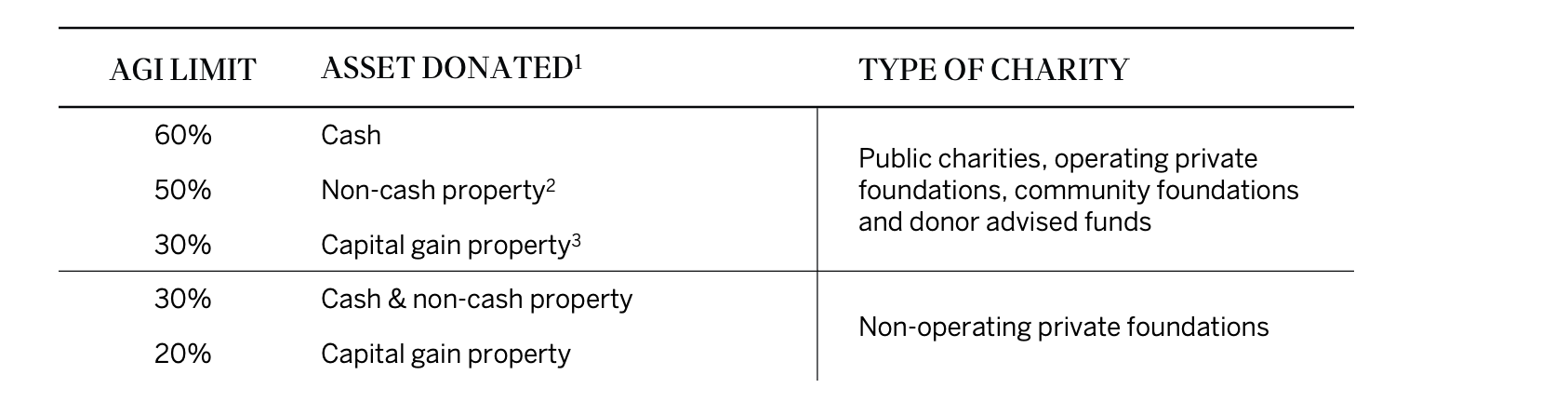

Changes to the Ordering of AGI Limits on Charitable Contributions

The OBBBA also changes the order in which the AGI limits are calculated for charitable contributions made after 2025. As general background, the following limits are applied to donations of distinct types of property to certain types of charitable organizations.

Currently, the deduction for cash contributions subject to the highest 60% AGI limit is calculated first; the 50% limitation deduction is calculated second and so forth. The new law reverses this ordering after 2025 so that the deduction for charitable contributions subject to the 20% AGI limit is calculated first and the 60% AGI limitation is calculated last. In addition, in 2026, the new charitable floor amount is subtracted from the charitable contributions of the lowest order calculation before determining the AGI limitation.

Any charitable contribution exceeding the applicable AGI limitation, plus any floor amount subtracted from the deductible portion of the contribution, may be carried forward and deducted, subject to the same limitations, for up to the following five years. If contributions do not exceed the AGI limitations, the floor amount is subtracted in the year the contributions are made.

Combined Impact

Combining the previous examples that illustrate the impact of the floor and the AGI limits on charitable contributions as well as the cap on itemized deductions, assume married taxpayers with an AGI of $1,000,000 in 2026 intend to donate cash of $100,000 to public charities and $200,000 of Nvidia stock held long-term to their Donor Advised Fund (DAF). For this example, also assume they can deduct $10,000 of State and local taxes.

The charitable deduction floor amount is $5,000 ($1,000,000 * .005), which reduces the deductible amount of the appreciated stock donation to $195,000 ($200,000 – $5,000). The 30% AGI limit applicable to the appreciated stock contribution is $300,000 ($1,000,000 * 30%). Therefore, $195,000 of the stock contribution is deductible. Next, the cash contribution AGI limitation is $405,000 ($1,000,000 * 60% = $600,000 – the $195,000 stock contribution deduction), so that the entire $100,000 cash contribution is also deductible.

Finally, the itemized deduction cap reduces the total itemized deduction from $305,000 ($295,000 charitable + $10,000 state and local taxes) to $291,573 ($305,000 – $13,427). The total combined reduction in the itemized deductions of $18,427 ($310,000 – $291,573) is lost forever and may have been avoided by accelerating the charitable contributions into 2025 before the effective date of the change in the law.

Using Appreciated, Concentrated Stock Holdings to Achieve Charitable Giving Goals

While a higher AGI limit applies to cash contributions, there is generally an overriding benefit in donating appreciated, publicly traded securities, at least up to the 30% AGI limit for such donations. Donating appreciated securities provides a deduction equal to the fair market value of the stock, avoids taxes on the unrealized capital gain, and reduces a concentration risk in the security. Giving appreciated securities can also preserve your cash for future distributions, expenses, portfolio rebalancing, or other uses.

We recommend that any taxpayer who makes charitable gifts consider using a highly appreciated security such as Nvidia for the donation, particularly if the security has become a concentrated position in the taxpayer’s portfolio. If this is done before the end of 2025, the deduction will not be subject to the 0.5% AGI reduction or the cap on total itemized deductions discussed above.

To illustrate, using a simple example, assume a taxpayer with $1,000,000 of AGI desires to give $300,000 to their DAF in 2025. This donation can then be doled out to charities from the DAF over time. The taxpayer compares donating $300,000 cash to donating $300,000 of Nvidia stock with a cost basis of $10,000. The taxpayer’s combined ordinary income tax rate (federal and state) is 45%. The taxpayer’s combined capital gains tax rate (federal and state) is 30%. Here is the comparison:

Cash donation of $300,000

Value of the tax deduction: $135,000 ($300,000 * 45%)

Net “cost” to the taxpayer: $165,000 ($300,000 – $135,000)

Stock donation of $300,000

Value of the tax deduction: $135,000 ($300,000 * 45%)

Value of the capital gains tax savings: $87,000 (($300,000 – $10,000) * 30%)

Net “cost” to the taxpayer: $78,000 ($300,000 – $135,000 – $87,000)

If stock concentration were not an issue, the taxpayer could use the available cash to buy back the same stock that was donated to charity, with a new tax basis equal to the fair market value of the stock on the date of purchase.

Limited Charitable Deduction for Non-Itemizers

Taxpayers who claim the standard deduction on their tax returns may deduct claim a charitable deduction of up to $2,000 for married taxpayers filing jointly or up to $1,000 for all other taxpayers.

Other Factors to Consider When Making Charitable Giving Decisions after OBBBA

The calculation of the charitable contribution deduction is complex. Factors such as your AGI, non-charitable itemized deductions, state income taxes, the assets you have available to donate, the type of charities you want to support, and your estimated income can all impact your potential tax deduction. The ability of taxpayers who have reached the age of 70-½ to make Qualified Charitable Donations of up to $108,000 (2025 amount) from their IRAs has not been impacted by the new deduction limits and should not be overlooked. A bunching strategy (making larger charitable donations in one year while claiming the standard deduction in other years) should also be considered when the charitable floor and cap limits are substantial.

Collaboration with your financial planner, portfolio manager, tax advisor, and sometimes legal counsel is even more important today when making decisions and executing your charitable giving goals. We recommend you ask your tax advisor to run the numbers to help determine the best strategy for you in any given year.

[1] Qualified conservation contributions of real property to a qualified organization, including a governmental unit and public charities, are limited to 50% of AGI (100% for qualified farmers and ranchers). Disallowed qualified conservation deductions can be carried forward for 15 years.

[2] Non-cash property is property other than cash or capital gain property and includes donations such as clothing, household items, electronics, food items, inventory, works of art, capital assets held one year or less, and capital assets for which the taxpayer elects to deduct the cost basis.

[3] Capital gain property is property that would result in long-term capital gain if it were sold at its Fair Market Value on the date it was contributed.

IRS CIRCULAR 230 DISCLOSURE

Pursuant to IRS Regulations, we inform you that any tax advice contained in this communication (including any attachments) is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax related penalties or (ii) promoting, marketing, or recommending to another party any transaction or matter addressed herein.

LEGAL, INVESTMENT & TAX NOTICE

The information contained in this presentation is of a general nature and does not consider the circumstances of any particular recipient. This information is

not intended to be and should not be treated as legal advice, investment advice, or tax advice and is for informational purposes only. Recipients should not under any circumstances rely upon this information as a substitute for obtaining specific legal or tax advice from their own counsel. All information discussed herein is intended to be current only as of the date of publication.

Tune in to CNBC’s #HalftimeReport at 12 p.m. ET today to hear our Chief Investment Officer, Amy Raskin, share her perspective on the latest financial market news.

We’re proud to congratulate Deb Gandy, Senior Managing Director and Wealth Advisor at Chevy Chase Trust, on being named a 2025 Women in Leadership Awards honoree by Virginia Business magazine.

This prestigious award celebrates women executives for their professional achievements, civic engagement, mentorship, leadership and breaking glass ceilings. Deb joins an exceptional group of honorees who are making meaningful contributions to their organizations and communities, while inspiring the next generation of women in leadership.

Deb will be recognized in the October issue of Virginia Business and featured online at VirginiaBusiness.com. The award was announced in July 2025 based on lifetime achievement and will be presented at a ceremony on October 6, 2025.

Chevy Chase Trust submitted an application fee to participate.

Our approach seeks opportunities across asset classes and around the globe. Perhaps our single most important distinction is this: At Chevy Chase Trust, we invest in global themes. We build equity portfolios of companies positioned to exploit powerful, secular trends, disruptive ideas, innovations, and economic forces.

The smartest investment strategies are informed by sound financial planning. Our clients appreciate an integrated approach and the difference it can make. Explore the difference in our financial planning, thematic investing, risk management and fixed income strategies.

Sometimes the greatest returns come from investing in people.

We’ve created a culture that values service over products, long-term goals over short term quotas, and your success over anything else. Our team of 90 professionals is comprised of CFAs , MBAs, CFPs® and other specialists in global research, thematic investing and planning.