Second Quarter, 2026

Click here for a printable version of the Investment Update.

Excessive optimism about AI has led to higher corporate profits and U.S. equity prices. We fear that expectations for uninterrupted exponential AI-related earnings growth have risen too far and too fast. We see better opportunities in several unloved areas both within and outside of the U.S.

BE WARY OF THE CROWD AT EXTREMES

Exceptionally strong earnings growth powered global equity markets to all-time highs in the second quarter, despite inflation and recession fears stoked by the conflict with Iran. The S&P 500 crossed 7,500 for the first time, generating a 15.2% total return for the quarter that made its 5% pullback in the first quarter seem like a distant memory. In the first half, the S&P 500 returned 10.2%, and the MSCI All-Country World Index generated an even more impressive 11.5% return.

Outside the U.S., earnings gains were solid and appear sustainable. U.S. earnings growth was eye-popping, mostly due to AI-related stocks. We fear expectations for future U.S. earnings are rising too far and too fast.

OVER EARNING?

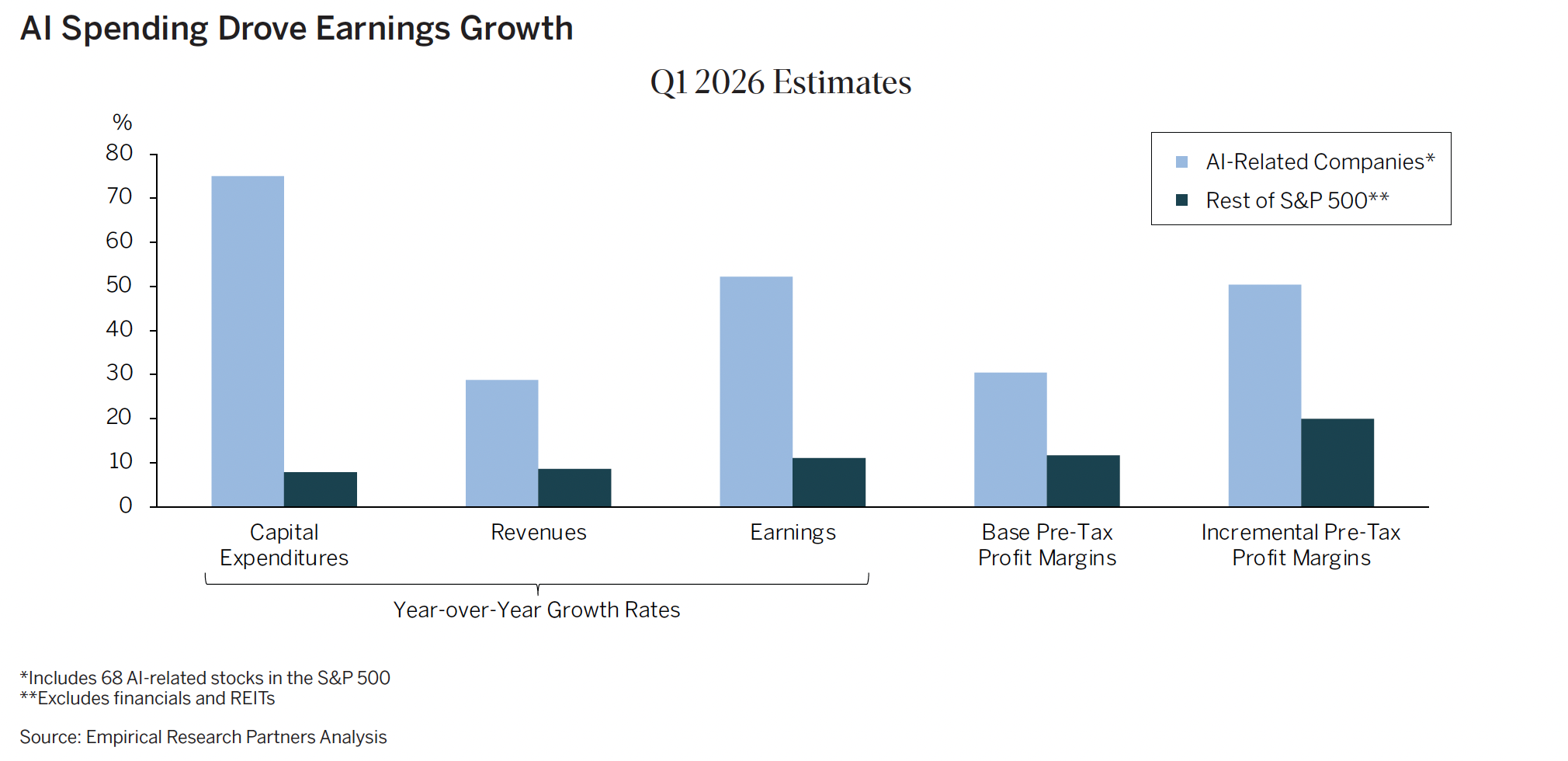

Robust earnings momentum in the U.S. is no longer confined to the Magnificent 71 stocks, the market darlings of recent years. Consensus earnings growth has been strong across sectors. But solid expected earnings growth for the median S&P 500 stock of roughly 14% is dwarfed by the torrid pace of earnings growth expected for AI-adjacent stocks. And because market capitalizations for AI-related stocks have ballooned in recent years, earnings growth expectations for the S&P 500, weighted by market capitalization, are a lofty 33% for 2026. Earnings growth estimates of approximately 16% for 2027 indicate investors expect the good times to roll.

Earnings growth of 16% after a year of 33% growth is a lot to ask of an expansion heading into its seventh year. It has never been done before. Bullish observers could argue, however, that past cycles haven’t had a gale-force wind from AI-related capital spending at their backs.

AI EVERYWHERE ALL AT ONCE

Our research suggests that AI-related earnings growth is likely to slow for several reasons.

New production capacity coming online: Over the next few years, additional capacity will ease the shortages of semiconductors and power-generation equipment that allowed producers to increase prices substantially. Upward revisions to Nvidia’s and Micron’s earnings alone represented over half of the S&P’s EPS2 rise year to date. More balanced supply and demand is likely to moderate earnings growth for many producers. We expect this to end the first uptick in technology prices in four decades.

CapEx accounting tailwind set to reverse: Today, both suppliers and buyers of AI hardware benefit from an accounting convention related to capital spending. When Nvidia sells an additional GPU or Micron sells an extra memory chip, they recognize both revenue and profit from the sale right away. Their customers, however, don’t immediately expense the entire purchase, which would reduce their profits. Instead, they treat these transactions as capital expenditures that they depreciate over time.

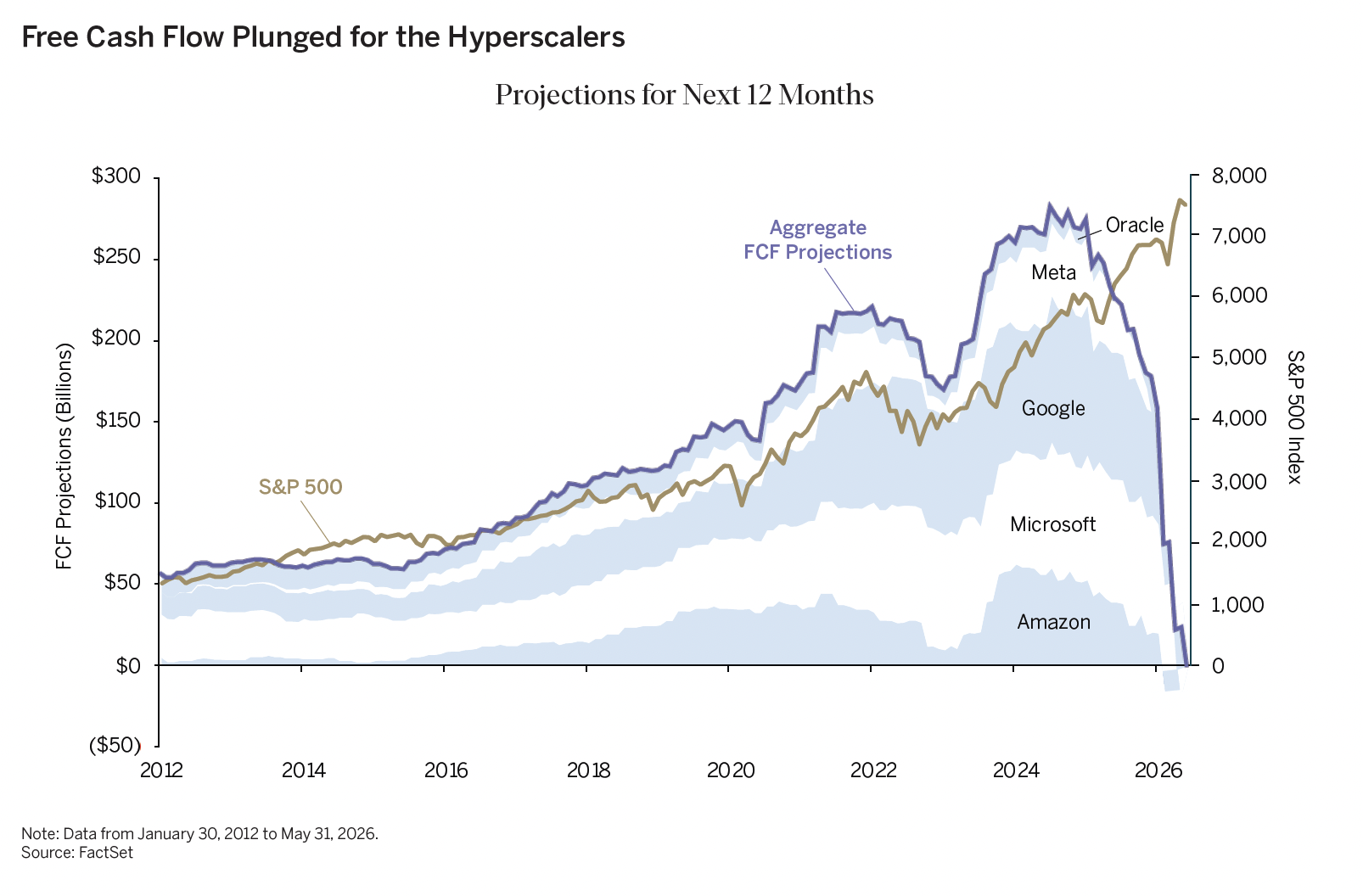

This timing mismatch creates an illusion of greater aggregate profits today and sets up conditions for disappointing aggregate profits in the future. At the current run rate, depreciation and amortization expenses for the hyperscalers that manage massive data centers will almost double from current levels in just two years, reducing their reported profit growth.

The pace of spending on AI gear may slow: Capital spending by the hyperscalers rose seven-fold in just the last eight quarters. It nearly doubled in the first quarter versus the first quarter of 2025. When companies spend so much at such a furious pace on scarce equipment that is rising rapidly in price, they seldom reap superior returns on capital.

Equity performance for the five main hyperscalers—Amazon, Microsoft, Alphabet, Meta and Oracle—lagged the U.S. market this year. As a group, these five stocks declined 8.5%, underperforming the S&P 500 by almost 19 percentage points in the first half. Their underperformance likely reflects a dramatic decline in expected cash flow, the result of their capital spending spree.

Investors may also be worried that the hyperscalers can no longer fund their rapid capital spending growth from the prodigious cash flows their other business units generate. As a result, they have been issuing massive amounts of equity and debt. Their combined equity issuance in the first half of 2026 exceeded the total for all of 2025. New equity issuance dilutes the value of their shares, while servicing additional debt reduces profitability and can limit firms’ flexibility in the future.

If the market continues to pressure their share prices, the hyperscalers may choose to rein in capital spending. This would hurt the earnings growth of their suppliers.

Lower AI spending could also slow economic growth. AI capital spending has been a growing driver of GDP, contributing approximately 0.8% to GDP growth in 2025 and over 1% this year. With real GDP growth expected to be 2.1% in 2026, AI-related spending may account for almost half of U.S. economic growth this year.

SHORT-TERM THINKING VERSUS LONG

The S&P 500 has generated a positive return in more than 80% of all rolling 12-month periods, so taking a bearish stance is rarely rewarded. But we are mindful of the advice of veteran financial analyst and author Ned Davis: “Be wary of the crowd at extremes.” With the current bull market surpassing the average in both duration and returns, several sentiment and valuation indicators signal poor long-term returns ahead.

We see several red flags that point to market extremes:

- The U.S. stock market’s capitalization is at a record high relative to gross domestic income.

- The value of IPOs and secondary market stock offerings has soared as companies have sought to take advantage of high stock prices.

- Rising margin debt and increased equity allocations point to keen investor appetite for risk.

- The S&P 500 is highly concentrated, with 38% of its capitalization in the Technology sector and 36% in the largest 10 companies.

- The S&P 500 was trading at 27.5x the last 12 months earnings at quarter end, higher than in over 94% of all readings since 1990.

Extreme markets often get more extreme before correcting. Thus, excessively bullish sentiment and valuations are poor indicators of short-term returns. At present, there is little evidence of a meaningful deterioration in earnings expectations, or that AI-related investment is generating excess capacity or driving a dangerous increase in corporate leverage.

But we cannot wait for such evidence to emerge before repositioning portfolios. In the last three major earnings booms for the technology sector, share prices peaked six to 10 months before forward earnings peaked, and stocks declined 30% on average before earnings estimates began to fall. Furthermore, when valuations are very high, as they are now, corrections tend to be severe.

AI OPTIMISM IS BEING TESTED TOO BIG TO FAIL?

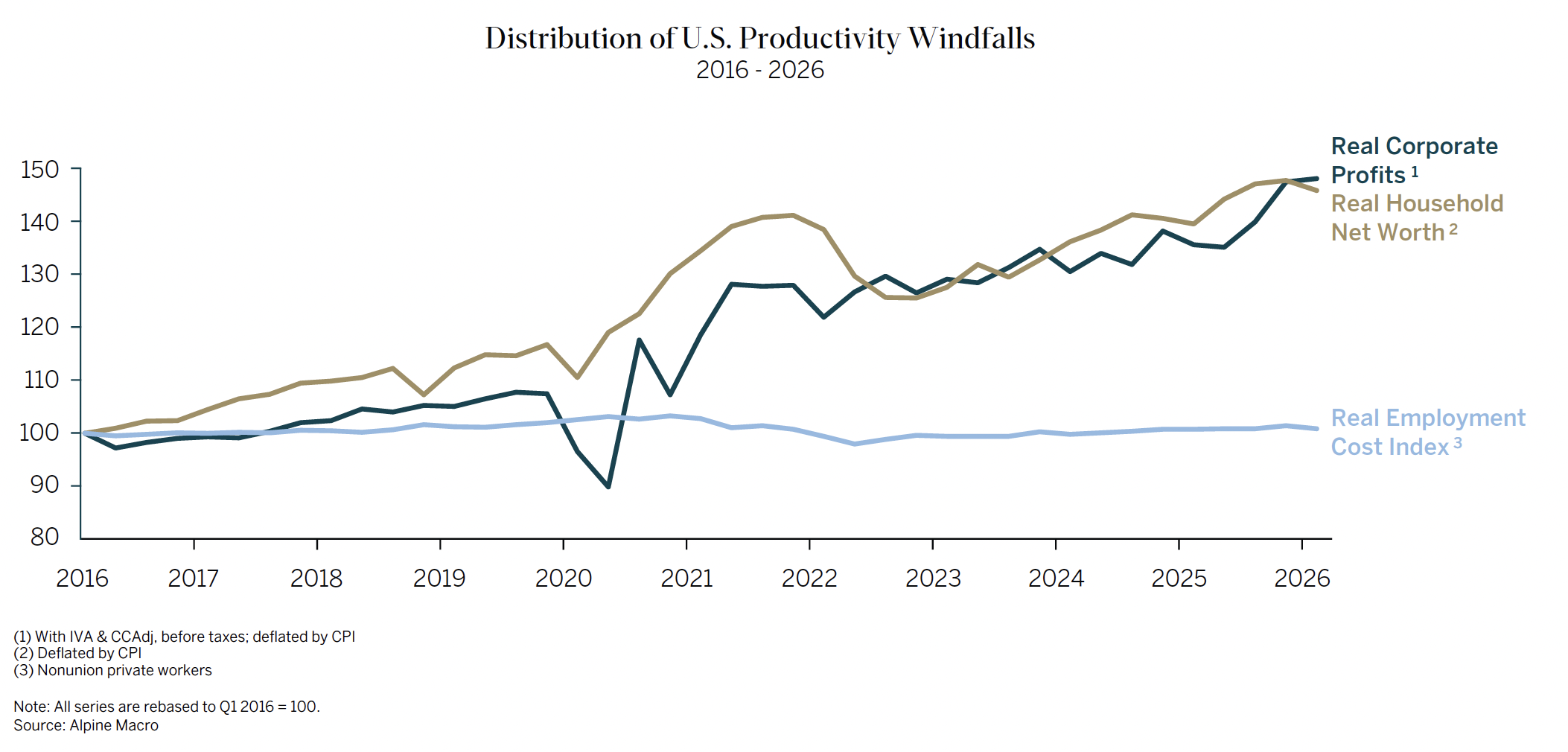

The impact of an equity market decline on the U.S. economy would be significant. After almost two decades in which wealth has grown faster than incomes, equity market appreciation has become an important driver of consumption.

Studies show that every extra dollar in equity wealth adds about three cents to consumption. U.S. household equity holdings now total about $73 trillion, up from $44 trillion in the third quarter of 2023. This change implies that U.S. consumer spending is likely 4% higher now than it would have been if stock prices had remained flat in this period. Indeed, consumer spending has grown faster than income for the past 24 months. Americans’ savings rate is near record lows.

More household wealth is tied to equities than ever before, and retirement savings are increasingly dependent on 401(k) and other defined contribution plans, rather than defined benefit pensions. As a result, the economic and psychological impact of market drawdowns is likely to be extensive. Because of the large weight of AI-related companies in broad U.S. equity market indexes, the health of the U.S. economy hinges, at least in part, on an uninterrupted rollout of and adequate return on AI.

OPPORTUNITIES ABOUND ABROAD, AGAIN

After lagging the U.S. equity market for many years, non-U.S. markets collectively took the lead last year. From January 1, 2025, through February 28, 2026, the MSCI ACWI ex USA generated a 48.3% return, almost 30 percentage points higher than the S&P 500’s return. The reasons for this outperformance include lower starting valuations almost everywhere, fiscal stimulus in certain European countries after a long period of austerity, and the imposition of U.S. tariffs, which encouraged an increase in ex-U.S. trade.

The war in Iran interrupted that non-U.S. market leadership. In the four months since the war began, the U.S. has outperformed, for two main reasons: First, the war drove up energy prices, which typically hurts Europe and Asia’s economies more than the U.S. Second, fear that the war would lead to a recession or high inflation led investors to buy technology stocks, which are seen as less sensitive to economic shifts.

These wartime arguments for increasing exposure to U.S. and technology assets lost force when both sides agreed to a ceasefire. Although there have been skirmishes since the Memorandum of Understanding was signed on June 17, we agree with the consensus view that President Trump wants to end the war, bring down gasoline prices and reposition his policies before the midterm elections.

Oil prices have declined nearly 40% from their wartime high. We do not expect them to decline dramatically from current levels. Inventory rebuilding is likely to drive strong demand, and war-related damage to production assets will limit supply. In our analysis, oil prices in the range of $65 to $85 are sufficient to support renewed outperformance by non-U.S. markets.

PORTFOLIO POSITIONING: OUR INVESTMENT THEMES

We have underweighted the technology sector for quite some time now, but it still represents a large share of client holdings. Given the risks presented above, we will likely reduce tech weights even further over the months to come. While we recognize the risk of selling too early, we feel this move is prudent, given the price rise in these holdings and the potential downside, if AI fervor subsides. Many of these holdings fall in our Rise of Purpose-Built Tech theme.

We are likely to continue to add to positions in our Advent of Molecular Medicine theme, which showed signs of strength after treading water for months. We were also pleased with our Next-Generation Automation theme. Valuations are rising for many of our holdings in this theme, but we think there is still more upside ahead.

We will likely increase holdings in our Opportunities Abound Abroad theme, particularly in companies that traded off the most during the Iran war. Finally, we are carefully evaluating the sizes of non-thematic positions we hold to provide diversification and manage risk. We try to keep this group of holdings to less than 25% of portfolios and have done so for most of the past decade. If AI-related stocks trade off sharply, however, we expect the portfolio weight of these diversifiers to increase, adding balance that could help preserve wealth.

CONCLUSION

More than 50% of U.S. equities are now held in index funds and other passively managed instruments, which tend to reinforce trends. A stock that rises in price becomes a bigger share of the index, prompting both passive and active managers to buy more, lest they take on too much benchmark risk. These purchases drive up the stock price further, increasing its market capitalization even more. However, this process can also work in reverse, with price declines reducing index weight, and thereby prompting sales.

Long-time investor Howard Marks has noted: “Value is what you get when you make an investment. Price is what you pay for it.” In certain areas of the current market, value and price seem unusually misaligned. As an active manager, when we think the market is not appropriately balancing risk and reward, we have the freedom to maneuver. We take this responsibility seriously and act accordingly.

(1) Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla

(2) EPS: Earnings per Share

Important Disclosures This commentary is for informational purposes only. The information set forth herein is of a general nature and does not address the circumstances of any particular individual or entity. You should not construe any information herein as legal, tax, investment, financial or other advice. Nothing contained herein constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments. This commentary includes forward-looking statements, and actual results could differ materially from the views expressed. Materials referenced that were published by outside sources are included for informational purposes only. These sources contain facts and statistics quoted that appear to be reliable, but they may be incomplete or condensed and we do not guarantee their accuracy. Fact and circumstances may be materially different between the time of publication and the present time. Clients with different investment objectives, allocation targets, tax considerations, brokers, account sizes, historical basis in the applicable securities or other considerations will typically be subject to differing investment allocation decisions, including the timing of purchases and sales of specific securities, all of which cause clients to achieve different investment returns. Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment or investment strategy will be profitable, equal any historical performance level(s), be suitable for the portfolio or individual situation of any particular client, or otherwise prove successful. Investing involves risks, including the risk of loss of principal. The level of risk in a client’s portfolio will correspond to the risks of the underlying securities or other assets, which may decrease, sometimes rapidly or unpredictably, due to real or perceived adverse economic, political, or regulatory conditions, recessions, inflation, changes in interest or currency rates, lack of liquidity in the bond markets, the spread of infectious illness or other public health issues, armed conflict, trade disputes, sanctions or other government actions, or other general market conditions or factors. Actively managed portfolios are subject to management risk, which involves the chance that security selection or focus on securities in a particular style, market sector or group of companies will cause a portfolio to incur losses or underperform relative to benchmarks or other portfolios with similar investment objectives. Foreign investing involves special risks, including the potential for greater volatility and political, economic and currency risks. Please refer to Chevy Chase Trust’s Form ADV Part 2 Brochure, a copy of which is available upon request, for a more detailed description of the risks associated with Chevy Chase Trust’s investment strategy. The recipient assumes sole responsibility of evaluating the merits and risks associated with the use of any information herein before making any decisions based on such information.